Real estate investing can be daunting, given the amounts of money involved and potentially having to run your investments as a business. To select the best investments, real estate investors look at a variety of criteria to influence their strategies and selection process.

Successful real estate investors leave emotion out of their decision-making process and leverage numbers to influence their investment decisions. They compare properties based on their financial merit rather than on looks or emotional attachment. This process is often referred to as deal analysis.

But what numbers? What key performance indicators do real estate investors look at to determine whether an opportunity is a good deal or a pass? Whether an acquisition is doing well or in trouble?

Here are the ten essential metrics of real estate investing. Master these, and your investing strategy will become coherent, comprehensive, and purposeful.

The net operating income (NOI) is the gross operating income (total revenue produced by a property) minus the operating expenses, calculated over the course of one year.

Operating expenses include property taxes, insurance, repairs, utilities, and any administration and management costs. Operating expenses do not include mortgage payments. Make sure you do not include principal or interest in your operating expenses when calculating NOI.

You may also be able to omit major capital expenditures from your operating expenses (replacing a roof, complete redo of the electrical system, etc.)

NOI is a crucial component in cap rate calculations, which we discuss next.

The calculation for NOI is as follows:

NOI = Gross Operating Income - Operating Expenses

You can read this article to learn more about how to use NOI.

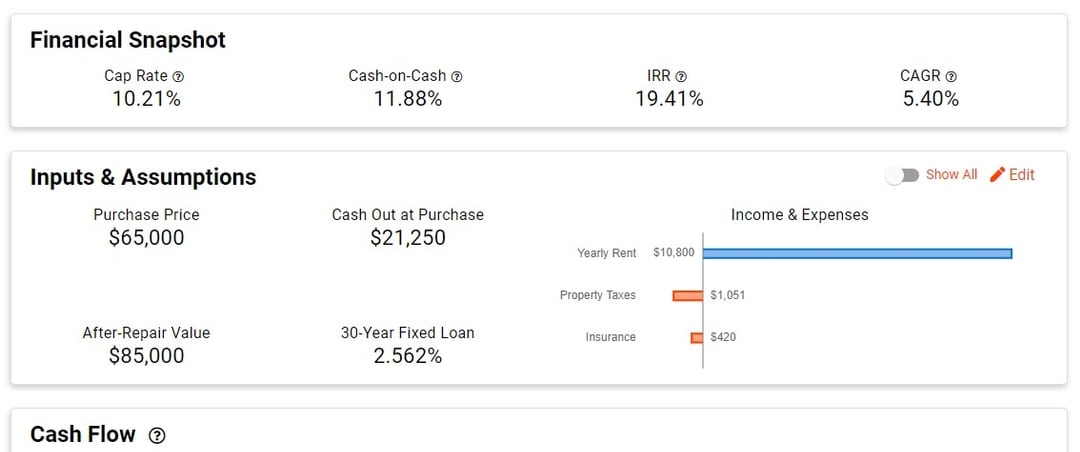

The capitalization rate (cap rate) is one of the most popular investment metrics. It is a percentage that measures the expected yield of a property over the course of a year, assuming it was purchased in cash.

The cap rate is best used to compare the performance of similar properties in the same market. It should be used in combination with longer-term metrics such as IRR because on its own, the cap rate does not account for a mortgage, the time value of money, or future cash flow of your property.

Prevailing cap rates usually range between 4% and 10%. A lower cap rate could indicate a market with higher property prices and/or lower rents.

The cap rate calculation works like this:

Cap Rate = NOI ÷ Property Value

Many investors buy property with the intent to raise the NOI—either by increasing revenue, decreasing expenses, or both. According to the cap rate calculation, this can force the value of the building higher, allowing the investor to reap more appreciation when they sell.

You can read this article to learn more about how to use cap rate.

Similar to the cap rate, the gross rent multiplier (GRM) is another way to evaluate the potential yield of an income-generating property. The GRM compares the gross operating income of a property compared to its price. Unlike the cap rate, the GRM does factor in the operating expenses.

The GRM is again best used in comparing similar properties in the same market and should be used in conjunction with longer-term metrics such as IRR.

Lower GRMs usually point to older properties with deferred maintenance and are an interesting strategy for investors looking to perform upgrade on their new investments. Higher GRMs generally point to newer properties which could require less maintenance.

The calculation works like this:

GRM = Gross Operating Income ÷ Property Value

The cash flow is the amount of profit that an investment property generates after all expenses, including mortgage payments and setting aside reserves, have been subtracted from the income. In other words, it is the amount of money that you expect to receive from or pay into the property every month or year.

Many real estate investors consider cash flow as one of the key metrics to evaluate a property and usually set a minimum amount that they are willing to accept on any given prospect.

Cash flow is calculated as follows:

Cash Flow = Gross Operating Income – Operating Expenses – Debt Service – Maintenance Reserves

The cash-on-cash return (CoC) is the percentage return on the cash you invest in a property measured using the cash flow. The cash used to buy the property commonly includes the down payment, closing costs, and any outlay for initial repairs or renovation.

The cash-on-cash return fluctuates based on your yearly cashflow and it is worth combining it with a long-term metric like IRR to get a full picture for your potential returns.

Note that all-cash buyers (no mortgage) put a lot more money in, so their CoC on the same property will be lower.

Many investors use CoC to evaluate whether they are better off with their money in a real estate deal vs. another investment vehicle, like a savings account or a stock portfolio.

CoC is calculated as follows:

Cash-on-Cash Return = Cash Flow ÷ Initial Cash Investment

You can read this article to learn more about how to use CoC return.

The internal rate of return (IRR) estimates the long-term return-on-investment by taking into account the cash flows over the years, the time value of money, and the opportunity cost of having your money tied up in this investment.

IRR is a great way of comparing a real estate investment to other potential investments — for example, buying a rental property vs. buying an online store – because IRR can estimate returns for any investment.

The calculation of IRR is complicated as it requires finding the interest rate at which all projected cash flows produce a net present value of zero. You can use Padvest to automatically calculate the IRR for the properties that you evaluate.

You can read this article to learn more about why IRR is important for investors.

The operating expense ratio (OER) measures the cost of operating a real estate investment compared to its income potential. It is calculated by taking the total operating expenses (not including mortgage payments and capital expenditures), subtracting depreciation, and dividing the result by the gross operating income.

The OER can give you a sense of how a property is performing before you buy. The operating expense ratio is most useful in comparing the performance of similar properties to understand how they perform.

If the expenses are 40% of the income, some investors see this as “too good to be true” and they are wary. By contrast, an OER of 60% or more might indicate that the property is over-managed and could experience reduced expenses through more efficient management.

OER is calculated as follows:

OER = (Operating Expenses – Depreciation) ÷ Gross Operating Income

The debt service coverage ratio (DSCR) is a measurement of an investor’s ability to pay their mortgage. It is calculated by dividing the NOI by the total proposed debt service.

If this calculation results in a number greater than one, the investor should be able to afford their mortgage with cash flow leftover. For example, a DSCR of 1.25 means that for every dollar spent on the mortgage payment, the investor should have $0.25 leftover as cash flow.

If the DSCR is less than one—say, 0.99 or lower—this means that the investor has to draw from an outside source to cover their mortgage. A lender is unlikely to lend on a deal that shows a DSCR below 1.25 on the underwriting.

DSCR = NOI ÷ One Year of Mortgage Payments

An investment property can become vacant when there is turnover in tenants. The vacancy rate is the percentage of time that the unit could be rented to the amount of time it is actually occupied.

The vacancy rate is used in calculating the gross operating income for the property. If it is set too low, the gross operating income becomes inflated. If set too high, a deal might look less desirable. It is important for an investor to understand local vacancy rates in the market where they are looking and based on their potential property type.

Padvest is a robust source of local data, including prevailing vacancy rates. Don’t rely on guesswork—check our data before you crunch the numbers!

The vacancy rate is calculated as follows:

Vacancy = Length of time a property is vacant ÷ Length of time a property is occupied

The loan-to-value ratio (LTV) is the amount of the property’s appraised value that a lender is willing to lend. Different lenders have different LTV requirements.

In construction loans, where the lender will be lending money to cover renovation or construction costs, this sometimes becomes the loan-to-cost ratio (LTC).

A lender who offers 75% LTV would lend up to $750,000 on a property that appraises at $1 million. The borrower would have to come up with the other 25% as a down payment, as well as any renovation costs.

LTV is calculated as follows:

LTV = Maximum Loan Balance ÷ Appraised Value

Shameless plug: Padvest automatically calculates and estimates most of the above metrics for you. It also allows you to compare various investments based on these metrics and even filter properties based on specific metric criteria. Give it a try!

We'll reach out to set up a call.